.png)

Read the latest company news and data-led articles about Web3, M&A, finance, and more.

Learn how restricted stock units work, vest, and get taxed so you know exactly what your equity is worth before and after it hits your account.

Q1 2026 saw 7,924 M&A deals totaling $861.1B in value. Here's what the data actually means for your strategy and where the smart money is moving in Q2.

Equity compensation pays employees in ownership, not just cash. Learn its many benefits, which plan fits a company's stage, and how each type is taxed.

RWA perps let you trade gold, stocks, and forex on-chain, 24/7, with leverage. No broker. No expiry. Here's how they work and why volume is exploding.

Perpetual swaps hit $705B in volume in March 2026. Learn how they work, why they dominate crypto trading, and where the real investment opportunities are.

Dive deep into the Whys and the Hows of structuring crypto incentives to attract and retain talented blockchain professionals.

Tether made $10B in 2025 while Circle made $2.7B. See exactly how stablecoin issuers generate profit and how you can invest in these companies.

The CLARITY Act is a U.S. bill that would bring clearer rules and have a major impact on crypto trading, fundraising, disclosures, and market supervision.

DePIN lets everyday people own the infrastructure powering Web3. Learn how it works, which projects lead the sector, and whether the tokens are worth buying.

Governance tokens give you voting power over DeFi protocols worth billions. Learn how they work, what you can vote on, and whether they belong in your portfolio.

Get the crypto fundraising info you need for protocol token projects: SAFTs, token minting, DAO launches, and where to sell your tokens the right way.

Linea is the zkEVM layer 2 blockchain being tested by SWIFT. Learn how it works, who backs it, and how to buy LINEA tokens.

Particle Network is an L1 blockchain that enables users to have a single account compatible with any decentralized applications. Here's how it works.

Theoriq coordinates autonomous AI agents to execute DeFi strategies on-chain. Learn how the blockchain works, who's backing it, and where to buy THQ coins.

Prediction markets are a billion-dollar industry. Here's how they work, who's building them, and how they differ from traditional betting platforms.

Read the complete breakdown of crypto ad policies across major advertising platforms to learn what's allowed, what's banned, and how to stay compliant.

Compare common vs preferred shares to learn what they are, how they work, and which one actually makes sense for your portfolio (including private stocks).

A Special Purpose Vehicle is a legal entity created for a specific purpose. This article covers how SPVs work, who uses them, and why they matter.

Plasma is a high speed blockchain that features zero-fee USDT transfers, custom gas tokens, and confidential transactions for global stablecoin payments.

A seed round raises funds to move from prototype toward product-market fit. Get it right, and you set your business up for growth. Here's how to get it right.

We highlight the Katana x IDEX acquisition in which Acquire.Fi served as a sell-side advisor. Also, get a chance to meet our CGO at the Digital Asset Summit.

Canton Network is a Layer 1 blockchain with configurable privacy. Only relevant parties see what concerns them. Public chains show everyone everything.

Acquire.Fi advised IDEX on its acquisition by Katana, enabling the launch of Katana Perps, a native perpetual futures platform built for DeFi.

Crypto marketing compliance is full of landmines. This guide breaks down the rules for all marketing channels so you can avoid sanctions from regulators.

SAFE gives investors the right to receive equity when a triggering event occurs. Money now, shares later on IPO, priced equity financing round, or merger.

DORA compliance means following EU Reg 2022/2554. Financial and crypto institutions must stay resilient against cyberattacks, outages, and vendor failures.

MegaETH is an Ethereum Layer-2 blockchain with 10ms latency, 100,000 TPS, and full EVM compatibility so no Solidity rewrites needed.

Lava Network routes blockchain RPC traffic to the fastest, most reliable providers. It's the decentralized resilience layer of the on-chain economy.

EDD is intensive customer scrutiny for high-risk entities. It asks: where does the money come from, who do they really answer to, and does it all add up?

.jpg)

Read our complete guide to preparing a CIM: what it is, what goes inside, the best practices to make your document stand out, & a template you can follow.

From obscure tech to sovereign reserve asset, crypto's institutional era is here. Explore the forces shaping institutional crypto adoption in 2026.

Verifying whether a carbon credit was consumed or sold multiple times has been nearly impossible. Tokenized carbon credits solves this issue. Here's how.

This article covers the 5 common methods to accurately price a business for sale depending on its size, industry, and what stage it's at.

Learn 7 proven strategies to buy a business with no money down. From seller financing to SBA loans, earn-outs, and creative deal structures that work.

The Travel Rule requires VASPs to collect and pass along sender and recipient details with every crypto transfer to keep each transaction traceable.

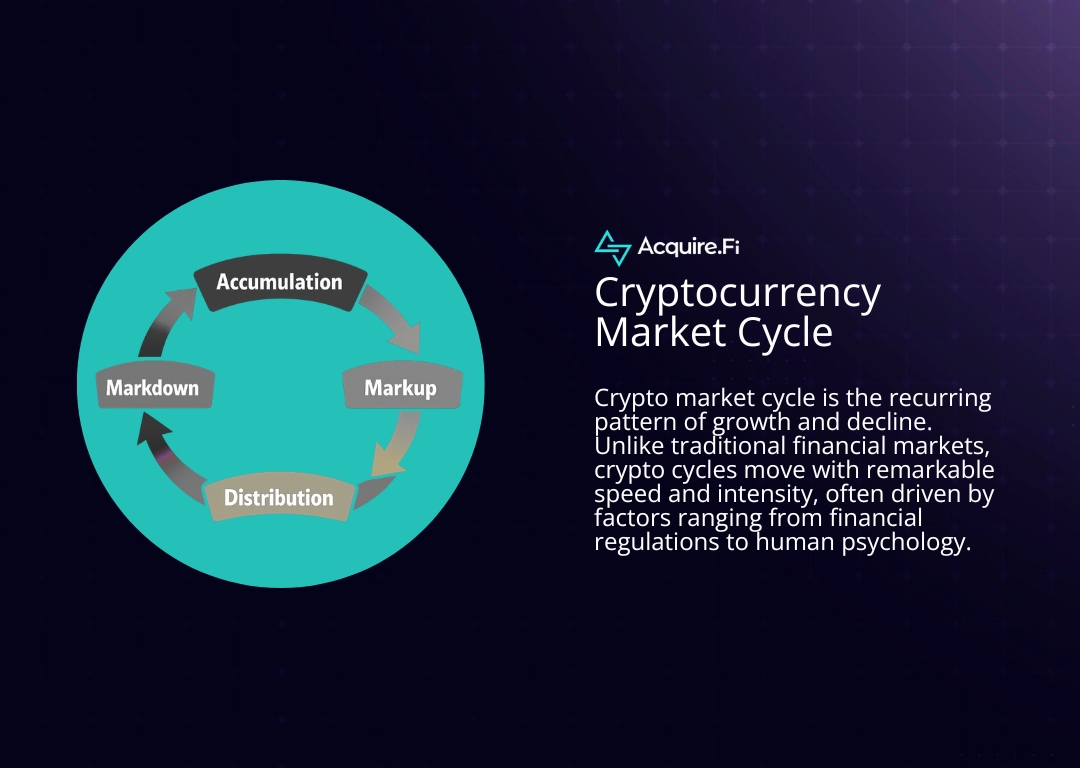

Crypto markets follow cycles. Its patterns repeat enough that traders have developed solid indicators to track market phases on which they base their moves.

The crypto market cycle is the recurring pattern of growth and decline. The cycle has four phases: Accumulation, Markup, Distribution, and Markdown.

Use this checklist to verify a Web3 project's claims and uncover hidden issues. Skipping due diligence risks overpayment or acquiring misrepresented assets.

MiCA is the EU's crypto regulation which protects investors while supporting innovation. Implementation is enforced in stages. Here's what changes in 2026.

This week, we briefly cover crypto M&A deals closed on January 2026 and the Digital Asset Market Clarity Act and its immediate effect in the industry.

Tokenized securities are stocks, bonds, & other traditional financial assets in digital form. Let's dive deep into how exactly tokenized securities work.

A tokenized RWA is a digital token representing ownership of tangible & financial assets. This guide covers how it works & adoption trends shaping markets.

Token distribution methods help raise funds and attract early users. This article highlights active and much-awaited TGEs and other token events in 2026.

As we start the new year, we want to take a moment to reflect on 2025 and share how we see the market evolving in 2026.

Zcash is a proof-of-work blockchain with optional privacy, letting users choose between public transactions or shielded ones that hide transaction details.

Distressed mergers & acquisitions refers to deals involving financially-troubled businesses. Buyers may acquire assets at bargain prices but face risks

We briefly look back at the Web3 M&A trends in 2025 & the macro-economic factors that affected deal activity & the crypto industry.

This week, we briefly talk about Robinhood's acquisition of an Indonesian brokerage and Binance's global exchange license.

Sei is an open-source blockchain featuring parallel processing to enable fast trading, low latency, and cryptocurrency exchange-focused applications.

Solana is a Layer 1 blockchain designed to process transactions in less than a second, with fees usually just a fraction of a cent.

Momentum is a decentralized finance (DeFi) protocol on the Sui blockchain designed to combine DeFi efficiency with institutional-grade infrastructure.

A crypto basket is a group of digital assets combined into one investment product. This post covers the different types and advantages of each one.

This week, we talk about one of the largest wallet-infrastructure deals of the year and how regulators have remained active across key jurisdictions.

This week, we cover the shifting crypto M&A landscape and how firms are adjusting to regulatory and market pressures.

In this newsletter, we cover crypto M&A acceleration despite Q4 volatility and highlight a hybrid perp exchange deal and a Tether equity OTC offering.

Learn how to decipher crypto charts and understand what the data means. While charts can't predict crypto price, they can help mitigate risks when trading.

This week, Coinbase acquired Echo while FalconX acquired ETF manager 21Shares. We also highlight profitable Web3 M&A and secondary market opportunities.

Risk-on assets are investments people tend to buy in a healthy economy. In this post, we cover the types of risk-on assets and cite examples for each.

We cover how crypto influencers help projects stand out and guide beginners on first use. Plus, dive deep into how they earn trust and shape user behavior.

We compare the various types of private equity, their approaches to different stages of business, risk profiles, and how they generate returns.

The secondaries market enables investors to trade existing assets with one another. This post covers the two types of secondaries + bonus crypto content.

MSB is a non-bank financial institution that facilitates movement or conversion of value its users.

Electronic money institutions, banks, & payment institutions help money move, but they differ.

An Electronic Money Institution (EMI) is a legal entity authorized to issue electronic money.

We cover Circle's IPO and highlight the M&A deal of the week and buy-side request for an EMI.

Avail Project acquired Arcana Network, the startup behind chain abstraction protocol and wallet SDK.

Altseason is when altcoins outperform Bitcoin. Learn key signs, timelines, and strategies to prepare for the next big crypto rally.

Cryptocurrency liquidity providers preserve market stability by bridging supply and demand.

Layer 1 refers to the base blockchain network and Layer 2 refers to secondary networks or protocols.

Crypto day trading is a fast-paced approach to trading digital assets.

Crypto marketing is the process of promoting blockchain-based projects, tokens, exchanges, or da

This week, institutional demand continues to drive a tidal wave of capital into crypto ETFs, with Ethereum ETFs outpacing Bitcoin across multiple metrics.

The acquisition serves to bolster Blockstream's Lightning, Liquid, and hardware wallet stack.

Launching a meme coin can be a thrilling way to combine internet culture with blockchain technology.

Lens Protocol is a decentralized, Web3-native social graph built on the Polygon blockchain.

DeFi has reshaped how we earn yield, trade assets, and access credit without relying on traditional banks.

Crypto algorithmic trading is a method that utilizes pre-programmed software to facilitate the buying and selling of digital assets based on predetermined rules.

In this week's newsletter, we're proud to announce that Acquire.Fi has helped facilitate the Vertex Protocol and The Ink Foundation M&A.

Market makers are essential participants in crypto exchanges for liquidity

Game studio Zelgor acquires Mixie AI to power no-code blockchain games and expand its creator-focused Web3 platform.

This week, we cover Circle’s $42B June 2025 IPO and how it ignited a Web3 IPO wave and a shift from tokens to regulated equity.

DeFi staking is the process of locking crypto assets into a Proof-of-Stake blockchain to support the network. Participants receive rewards in return.

Bitcoin price has dropped due to geopolitical tension, a stronger dollar, and Fed interest rate decisions. Bitcoin’s short-term outlook appears uncertain.

Get clarity on SAFE, SAFE+T, and SAFT fundraising instruments and discover how Web3 startups use them for early-stage funding and compliance.

Learn how crypto farming works, yields, and risk factors. We also list popular yield farming protocols where you can earn passive token income.

This week, we cover how crypto presales are increasingly starved for capital as the over-the-counter (OTC) market siphons off available liquidity.

Learn how to secure funding for a startup using ten proven routes such as crowdfunding, SBA loans, venture rounds, and government grants.

Crypto markets never sleep. Discover how price and technical alerts help swing traders, scalpers, and HODLers react fast in volatile markets.

In this week's newsletter, we discuss a flurry of high-profile deals in 2025, starting with Coinbase' acquisition of Deribit.

Here's a list of the best crypto trading bots based on our tests

Let's find out if an Initial Coin Offering (ICO) is a good investment

This is a comparison between spot trading and futures trading.

This is a comparison between perpetual futures vs spot trading.

Here's a list of some of the trends in Web3 game development

Analyze the impact of tariffs on crypto for investors to make better financial decisions.

Knowing the primary and secondary markets is important if you want trade or access newer ones.

Explore crypto friendly banks, their features, & how investors and businesses are catered.

An analysis of top altcoins poised for growth in 2025 and beyond

Here's a list on the leading RWA coins to consider based on market capitalization

Read our complete guide to preparing a CIM: what it is, what goes inside, the best practices to make your document stand out, & a template you can follow.

This article covers the 5 common methods to accurately price a business for sale depending on its size, industry, and what stage it's at.

Learn 7 proven strategies to buy a business with no money down. From seller financing to SBA loans, earn-outs, and creative deal structures that work.

Use this checklist to verify a Web3 project's claims and uncover hidden issues. Skipping due diligence risks overpayment or acquiring misrepresented assets.

Distressed mergers & acquisitions refers to deals involving financially-troubled businesses. Buyers may acquire assets at bargain prices but face risks

Mergers and acquisitions are pivotal strategies used by companies to achieve growth ...

Web3, also known as Web 3.0, is the next evolution of the internet. It is a decentralized...

In the world of Web3 and decentralized technologies, mergers and acquisitions (M&A)...

Hostile takeovers are among the most dramatic and controversial events in the corporate...

This week, we briefly cover crypto M&A deals closed on January 2026 and the Digital Asset Market Clarity Act and its immediate effect in the industry.

We briefly look back at the Web3 M&A trends in 2025 & the macro-economic factors that affected deal activity & the crypto industry.

This week, we briefly talk about Robinhood's acquisition of an Indonesian brokerage and Binance's global exchange license.

This week, we talk about one of the largest wallet-infrastructure deals of the year and how regulators have remained active across key jurisdictions.

This week, we cover the shifting crypto M&A landscape and how firms are adjusting to regulatory and market pressures.

In this newsletter, we cover crypto M&A acceleration despite Q4 volatility and highlight a hybrid perp exchange deal and a Tether equity OTC offering.

This week, Coinbase acquired Echo while FalconX acquired ETF manager 21Shares. We also highlight profitable Web3 M&A and secondary market opportunities.

We cover Circle's IPO and highlight the M&A deal of the week and buy-side request for an EMI.

This week, institutional demand continues to drive a tidal wave of capital into crypto ETFs, with Ethereum ETFs outpacing Bitcoin across multiple metrics.

DORA compliance means following EU Reg 2022/2554. Financial and crypto institutions must stay resilient against cyberattacks, outages, and vendor failures.

The Travel Rule requires VASPs to collect and pass along sender and recipient details with every crypto transfer to keep each transaction traceable.

MiCA is the EU's crypto regulation which protects investors while supporting innovation. Implementation is enforced in stages. Here's what changes in 2026.

Analyze the impact of tariffs on crypto for investors to make better financial decisions.

The CryptoStrategic Reserve is a newly announced initiative by U.S. President Donald Trump.

With deep roots in traditional finance and the digital asset industry, Acquire.Fi operates as a specialist M&A advisory firm. Coverage spans M&A, secondaries, OTC, and capital markets advisory across digital assets and frontier tech. Our team has decades of combined experience across every stage of the deal lifecycle.

.webp)